CRM for microfinance organizations

The microloan business is always a fast-paced business: while one borrower is repaying a loan, another is extending the loan, and a third is delaying a payment. Everything here needs to be under control, as a successful microfinance company isn't one that issues more loans, but one that effectively manages data, builds long-term relationships with clients, and minimizes risks.

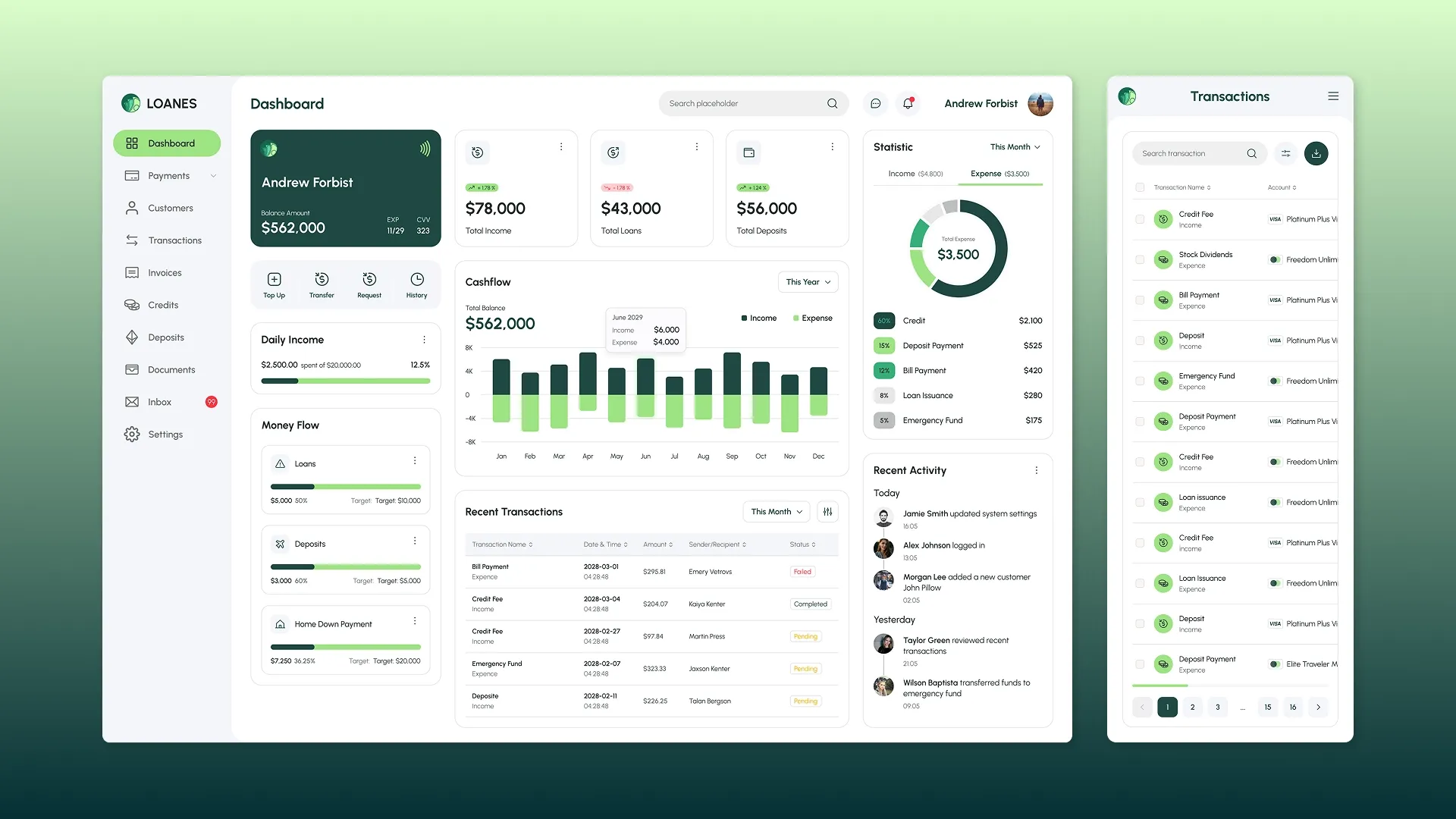

CRM for microfinance organizations is a key tool that integrates all processes into a single, manageable, and transparent system. This digital ecosystem helps make quick and informed decisions, automate routine tasks, and increase customer loyalty.

AvadaCRM offers CRM development services for microfinance organizations. With our proprietary software, you'll manage your business without endless phone calls, spreadsheets, and manual approvals, using a smart system that automates routine tasks and enables data management.

What is CRM for microfinance organizations?

A CRM for a microfinance organization is a customer relationship management system tailored to the needs and processes of microfinance firms, pawnshops, and credit bureaus. This program covers all processes: from initial contact with the client to full loan repayment or transfer of the case to debt collectors. It collects and analyzes data, helps automate audits, generates reports, manages marketing campaigns, and even supports integration with external services, such as government registries, credit reporting systems, and payment gateways.

Unlike generic CRM systems, custom-designed solutions take into account the specifics of the microloan industry: from borrower scoring and solvency assessment to automated payment schedule monitoring, interaction with debt collectors, and regulatory compliance.

What problems does automation solve for microfinance organizations?

Managing microfinance institutions requires maximum flexibility and transparency, balancing application processing speed with risk management. These organizations regularly face challenges that can be addressed with a custom CRM for microfinance institutions.

High workload on staff

Manually processing applications, calls, payments, and contract renewals takes a lot of time, effort, and attention. Microfinance organization management software helps relieve employees by automating applications, reminders, and notifications.

Insufficient control over processes

Without a unified system, data is scattered across departments. A CRM system for microfinance organizations (MFIs) consolidates all information into a single interface, providing management with a complete picture of the business's status.

Risk management

Assessing client creditworthiness is a critical step in the work of microfinance organizations. Integrating CRM with external databases (credit bureaus, state registries, scoring systems) enables faster and more accurate loan decisions.

Regulatory compliance

Microcredit organizations are legally required to store and process clients' personal data, submit reports on time, and record financial transactions. CRM for microcredit organizations simplifies these tasks with built-in policies and templates.

High customer turnover

Competition in the microloan market is rapidly increasing, and client retention is a particular challenge. A customized program can include tools for automated SMS and email notifications and bonuses for repeat borrowers.

Quick decision making

When a client urgently needs money, even an extra 15 minutes of waiting can cost you the deal. A CRM system for microfinance organizations eliminates delays by automatically processing applications, distributing tasks among managers, issuing reminders and notifications, and pulling up transaction history.

This microfinance organization (MFO) program eliminates the human factor from routine tasks, speeds up application processing, and reduces operational costs. It synchronizes the work of all departments, from customer service to security.

CRM functions for microfinance organizations

Each type of microfinance business has its own specifics, and therefore, different tasks that a CRM system must address. Depending on the specific business area, unique custom features are implemented into the system.

CRM for microcredit companies (microloans, microcredits)

Microfinance organizations issuing short-term loans require prompt decision-making and minimized risk of default. CRM for microloans includes tools that automate client assessment and loan management:

- Automatic client scoring based on credit histories and internal assessment rules;

- integration with payment systems for instant payments (for example, via LiqPay) automatic generation of QR codes for bill payment;

- Automatic generation and processing of applications from the website, mobile application, and call center;

- management of payment schedules, overdue payments, automatic reminders to clients via SMS, email, and push notifications;

- debt control, the ability to transfer cases to collection agencies via CRM;

- analytics on attraction channels, manager effectiveness, return and non-return rates;

- automatic distribution of applications between managers according to specified criteria (geography, amount, source of application);

- integration with electronic signatures for contactless signing of contracts;

- Setting up flexible loan decision-making rules—for example, rejecting applications if the client has more than two late payments in the past year.

CRM for pawnshops

Pawnshops handle valuable collateral and require strict accounting of each item, monitoring of storage periods, and transparent disposal of unclaimed collateral. The pawnshop program covers the entire collateral management cycle:

- accounting of collateral property with reference to photos, descriptions, assessments, and movement history (reception, return, sale);

- search for an item by barcode, serial number or other parameters;

- management of storage periods, interest calculation, automatic notification of clients about redemption dates via SMS/email/push;

- integration with an online store or website for selling unclaimed items;

- control of warehouse balances, generation of reports for each object, automation of printing of stickers/barcodes;

- integration with fiscal registrars and accounting programs;

- Automatic receipt printing and integration with fiscal registrars;

- formation of financial reports on revenue, marginality of goods sold, for each branch, manager, and area of activity.

CRM for credit unions

Credit unions operate with long-term loans and complex membership structures, so a CRM for this type of credit institution includes modules for managing not only finances but also interactions with shareholders:

- accounting of shareholders, their personal data, history of membership fees, credit load, participation history;

- management of loan issuance and repayment with the creation of individual payment schedules;

- automatic notifications about payments and debts;

- a module for organizing and recording meetings, voting, and handling appeals;

- reports on financial performance, loan portfolio management, forecasting reserve fund needs;

- status management – new, active, blocked, excluded;

- sending out notices of meetings, changes in rules, and voting results;

- integration with accounting programs 1C, BAS, SAP;

- formation of mandatory reports for regulatory authorities.

CRM for online microfinance organizations and fintech startups

Online microfinance organizations and fintech startups operate in a digital environment where speed of application processing, a high level of automation, and customer convenience are critical. CRM for online microfinance organizations is built around digital service channels and integration with external services:

- Automatic client scoring based on data from external sources (credit bureaus, social networks, digital profiles);

- Instant loan approval and disbursement completely online, without a visit to the office, and automatic transfer of funds to the client's card via the bank's API;

- integration with electronic signatures, state register APIs for data verification, and personal identification platforms (BankID, Diya, KYC providers);

- managing omnichannel communications with clients (chatbots, messengers, email, push);

- adaptive dashboards for monitoring key metrics in real time;

- A/B testing tools for offers and credit terms for flexible product customization;

- automation of anti-fraud control, monitoring of suspicious transactions;

- integration with loan issuance platforms via mobile applications;

- automatic triggered mailings (for example, “leave a request right now – get a percentage discount”);

- Setting up automatic limits based on geography, age, and client type.

With us, you'll receive a unique CRM system for any type of microfinance organization, tailored to the specifics of your business, ensuring flexibility, scalability, and full integration with your existing ecosystem.

Data security in CRM for microfinance organizations

For microfinance organizations, data security is not just a requirement, but the foundation of customer trust and legal compliance. We implement a comprehensive set of multi-layered security measures in our customized CRM systems:

- Server-side data encryption with modern algorithms (e.g. AES-256) protects both the information flow and static data;

- A two-factor authentication (2FA) system for all users of the CRM system for microfinance organizations reduces the risk of unauthorized access even if the password is compromised;

- Delimiting access rights reduces the risk of accidental or intentional information leaks, since employees see only the data and functions that are necessary for their work;

- audit logs and activity logs to track suspicious activity or reconstruct events;

- Scheduled data backups stored on isolated servers ensure quick recovery in the event of a failure.

Security in CRM for microfinance organizations is an important part of a strategy that encompasses both technological and legal components.

Stages of CRM system development

Developing a custom CRM system for a microfinance organization is a multi-stage process that requires developers with deep expertise and attention to detail. Our team maintains a transparent and customer-focused approach at every stage.

- Analysis and definition of automation goals

The first stage of developing a management system for a microfinance organization is an analysis of business processes, current tasks, and strategic goals. Analysts delve into the specifics of the company's operations: they study how applications are processed, client data is processed, payments and debts are tracked, and communication methods are utilized. It is important to identify bottlenecks that slow down operations or create risks and define the goals of CRM implementation.

- Technical specifications

Based on the analysis, a technical specification is created – a key document outlining all the requirements for the future CRM system. The specifications outline functional modules, integrations, user roles, use cases, and data security requirements. Non-functional parameters such as performance, scalability, and the number of concurrent users are also defined. The technical specifications are a project roadmap agreed upon by the development team and the client, eliminating misunderstandings and additional adjustments.

- Design and prototyping

After the specifications are approved, the system architecture is designed: key CRM components are defined, how they interact, the database selection, and the server architecture (monolith or microservices). Next, interactive screen prototypes are developed in Moqups, Figma, Axure, or Adobe XD to demonstrate to the client how the CRM will look and function before the project begins.

- UX/UI design development

UX/UI design is the visual and functional aspects of a program. Designers focus primarily on usability – the system must be intuitive for all employees, providing quick navigation, minimal clicks to complete tasks, and access to important data. The design takes into account corporate colors, the brand book, and modern trends such as minimalism, adaptability, and lightweight interfaces without unnecessary clutter. Special attention is paid to interfaces for mobile devices and tablets to ensure the system remains user-friendly even outside the office.

- Program code

A key stage of CRM development for microfinance institutions is programming code. To ensure fast operation and a flexible interface, front-end development tools such as React, Vue.js, and Angular are used. The back-end is implemented in programming languages such as Python and Java, using the Node.js platform, frameworks, and databases such as PostgreSQL, MySQL, and MongoDB. REST APIs or GraphQL are used for data exchange. At this stage, integrations with external services are implemented, interaction with the database is configured, and data security is ensured (e.g., through encryption, tokenization, and OAuth).

- Testing

After the code is written, the system undergoes multi-layered testing. QA engineers check the CRM for bugs, logic errors, and vulnerabilities. Comprehensive testing also includes load tests, integration checks, security, and usability. The goal is to release a stable and reliable product, ready to operate even under extreme load conditions.

- Release and implementation

This stage includes migrating the microfinance organization's CRM system to a server or hosting it in cloud storage, configuring domain names, SSL certificates, and databases. Final testing is conducted in real-world conditions, data is migrated from old databases, and employee training is completed. After the release, the CRM is gradually implemented to avoid disruption to business processes, but from day one, the system begins saving employees time and reducing your business's costs.

- Project support and development

Working with a CRM doesn't stop there; the program requires technical support, updates, and scaling as your business grows. After the system's launch, user feedback helps us monitor logs, troubleshoot issues, provide user support, and update libraries and server components to improve security. At the same time, we continue to develop the system, adding new modules, integrations, and interface improvements. This approach ensures the CRM remains relevant and provides maximum value to your business.

Why should you order a CRM system for microfinance organizations from AvadaCRM?

Creating an automated management system involves more than just programming, but also a deep dive into business processes, legal requirements, and the intricacies of financial transactions. It's best to order a CRM system for microfinance organizations from us because we:

- We have extensive experience in the fintech sector , including successful CRM implementation cases for physical and online microfinance organizations, pawnshops, and fintech startups. We understand their specifics – from calculating interest on loans to integrating with AML systems.

- We develop unique software products and adapt existing programs. We don't offer template solutions – each CRM system we develop is tailored to the specifics of your business, its scale, and strategic goals.

- We provide dedicated, professional teams of analysts, designers, and developers with extensive experience, who are up-to-date on the latest trends in the IT industry and possess a deep understanding of modern technologies;

- We value our clients' trust , so you will always be informed about the progress of the project, be able to make adjustments and receive reports on the work done;

- We'll be with you for the long haul – updating, scaling, and refining the system as your company grows;

- We use a modern technology stack to ensure that CRM is stable, scalable, and fast.

The AvadaCRM team doesn't just create software; it develops your own digital ecosystem that solves your problems, not creates new ones.

FAQ

-

Does the CRM system for microfinance organizations support the management of multiple legal entities or branches?

Within a single CRM system for a microfinance organization, it's possible to manage multiple companies and branches in a single system, with individual settings for each business, including reports, users, and financial indicators. This is extremely convenient for network microfinance organizations that require centralized management.

-

Is it possible to connect the system to POS terminals and cash register equipment?

Integration with POS systems and cash registers is possible via drivers or APIs. All financial transactions will then be recorded in the CRM in real time. This simplifies accounting, cash management, and reporting.

-

Can the program automatically generate reports for audits?

A CRM system for microfinance organizations can automatically generate reports in accordance with the requirements of regulators, tax authorities, or audit firms, export them in the required formats, and even send them on a schedule.

-

Is it possible to implement custom scoring rules into the program?

You can set up custom scoring models that allow you to define your own formulas, weighting factors, and criteria for evaluating borrowers.

-

Does the CRM support integration with instant messengers?

CRM can be integrated with popular instant messengers (WhatsApp, Telegram, Viber, Facebook Messenger, etc.) to communicate with clients, send reminders, offers, and notifications directly from the system.

-

Can the system automatically renew contracts and accrue interest?

The CRM can be enhanced with features for automatic contract renewals, interest recalculation, and client notifications. All processes will be executed according to preset rules without operator intervention.

-

Is there any control over loan issuance limits and automatic blocking?

In a customized CRM system, you can set limits on amounts, number of loans per day, client categories, regions, and other parameters, as well as automatically block new loans when these limits are exceeded.

-

Is it possible to integrate CRM with a call center and IP telephony?

Yes, the CRM can be linked to Asterisk, Binotel, and Zadarma, so that calls are recorded directly in the client's card, and call recordings are saved in the system.

-

How is CRM compliance with legal requirements ensured?

During development, we take into account current legal regulations (e.g., GDPR, personal data protection laws, and requirements for microfinance organizations) during the analysis and design stages. We implement legally binding data protection mechanisms, encryption, conduct user activity audits, and conduct regular security testing.

-

How is the CRM program adapted for a Ukrainian pawnshop?

Pawnbroker software is developed taking into account local legislation, collateral accounting requirements, customer service, and integration with cash register systems.